.jpg)

On March 6, 2024, the SEC issued a final rule to enhance and standardize climate-related disclosures for investors. The SEC's final rule mandates companies to disclose information regarding their governance structures, strategies, risk management practices, and metrics and targets related to climate-related risks and opportunities. This aims to provide investors with consistent, comparable, and decision-useful information to assess companies' exposure to climate-related risks and opportunities.

This article summarizes the changes introduced by the SEC's final rule and considerations for implementing the final rule.

The final rule requires the following climate-related disclosures:

Entities are required to include climate-related disclosures within their registration statements and Exchange Act annual reports. The disclosures under Regulation S-K, except for Scopes 1 and/or 2 emission disclosures, are required to be disclosed in a separate and appropriately captioned section of the registration statement or annual report, in another appropriately captioned section of the filing, such as Risk Factors, Description of Business, or Management’s Discussion and Analysis of Financial Condition and Results of Operations, or, by incorporating the disclosure by reference from another filing as long as the disclosure meets the electronic tagging requirements of the final rule.

For domestic registrants that are required to disclosure Scope 1 and 2 emissions, disclosure is required in its annual report on Form 10-K, in its quarterly report on Form 10-Q for the second fiscal quarter in the fiscal year immediately following the year in which GHG emissions metrics disclosure relates with reference to the Form 10-K, or in an amendment to its 10-K filed no later than the due date for the Form 10-Q for its second fiscal quarter. For foreign issuers, the disclosures are required in the Form 20-F annual report or amendment to its annual report on Form 20-F, which shall be due no later than 225 days after the end of the fiscal year to which the GHG emissions metrics disclosure relates. If an entity is filing a registration statement, the disclosures should be included in the registration statement as of the most recently completed fiscal year, which is at least 225 days prior to the date of effectiveness of the registration statement.

The final rules include a “safe harbor” provision that protects issuers from private liability for forward-looking climate-related disclosures. This safe harbor applies to transition plans, scenario analysis, the use of an internal carbon price, and stated climate targets and goals.

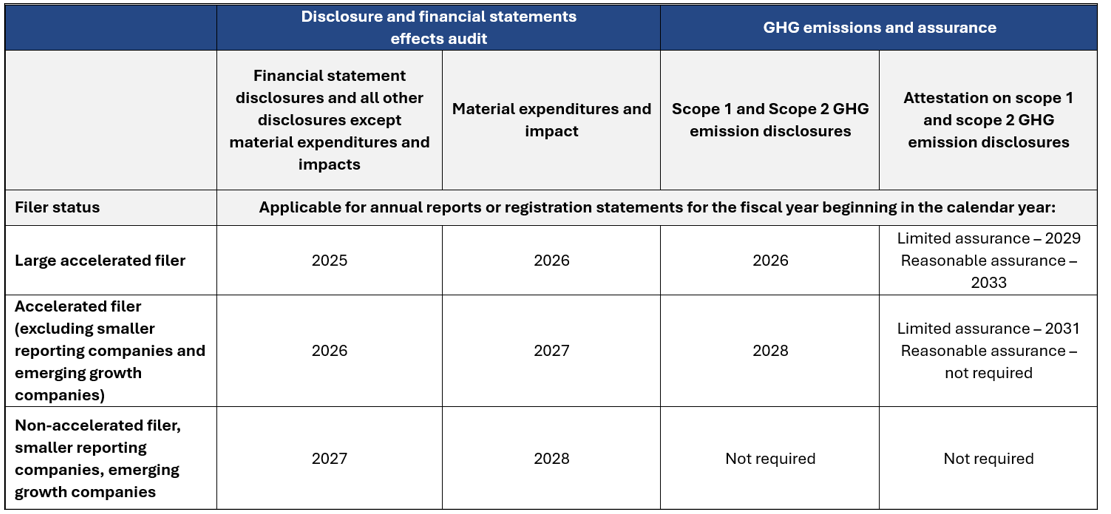

The final rules are effective 60 days after they are published in the Federal Register. Compliance dates for the rules depend on an entity’s filer status.

Entities should consider the following when developing their implementation plan:

Navigating the implementation of the SEC's final rule on climate-related disclosures requires careful planning, coordination, and attention to detail across the organization. Staying proactive and developing an implementation plan will contribute to the final rule's successful adoption.

Our team can help your company with its ESG objectives, from financial reporting assistance to internal controls over financial reporting considerations. Contact us to see how we can help.

Socorro Partners is the brand name under which Socorro CPAs & Advisors, LLC (a Florida, U.S. limited liability company) and Socorro Consulting, LLC (a Delaware, U.S. limited liability company) and its subsidiary provide professional services under an alternative practice structure in accordance with the AICPA Code of Professional Conduct and applicable laws, regulations, and professional standards. Socorro CPAs & Advisors, LLC is a licensed independent CPA firm that provides attest services. Socorro Consulting, LLC and its subsidiary are not licensed CPA firms and provide only non-attest services, including tax and consulting services.

The Socorro Partners logo, including the icon, and the “Look through the noise” tagline are trademarks of Socorro Consulting, LLC.

© 2026 Socorro Partners. All rights reserved.

All content on this website is the property of Socorro Partners. Unauthorized use is strictly prohibited. Content on the socorropartners.com website has been prepared for general information only and is not intended to be relied upon as accounting, tax, or other professional advice. You should consult with your professional advisors regarding your specific circumstances.